Fake account prevention

Streamline customer onboarding by identifying bad actors during account creation, reduce friction for legitimate customers and improve trust and safety in your platform.

Fake account prevention starts here

What is a fake account?

Fake accounts are developed using a stolen or synthetic identity (a combination of fabricated and real identity data). The bad actor may log onto the account and commit fraud immediately or mimic legitimate user behavior for years to build credibility before conducting account-driven fraud, scams or large breakout schemes.

Why are fake accounts created?

Cybercriminals create fake accounts to spread malware, seek loans, execute money transfers, launder money, gain credit, purchase products and services, influence product reviews and spread misinformation.

Why do you need fake account prevention?

By preventing these accounts from developing, organizations improve the trust and safety of their platform. Identifying stolen or fabricated information during the account building process prevents a fake account from being developed, safeguarding your organization, your legitimate customers and the payments ecosystem.

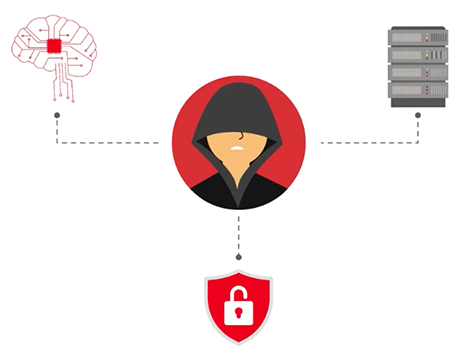

How fraudulent accounts happen

Fraudster creates account

Fraudsters develop accounts using stolen identity information or synthetic identities fabricated from a combination of real identity information.

Fraudster makes transactions

Fraudsters conduct transactions ranging from purchasing products or services to executing money transfers.

Fraudster logs onto account

Fraudster regularly log onto the account to mimic legitimate user behavior and build credibility. Once credibility is established, loans can be applied for and more accounts can be opened, depending on the strategy of the scammer.

The solution

Once bad actors have created a fraudulent account, they have a wealth of options at their fingertips. They could open new accounts to gain instant credit, launder money or generate value through promotional abuse, which can cause reputational damage to merchants’ platforms and result in chargebacks that eat into profits.

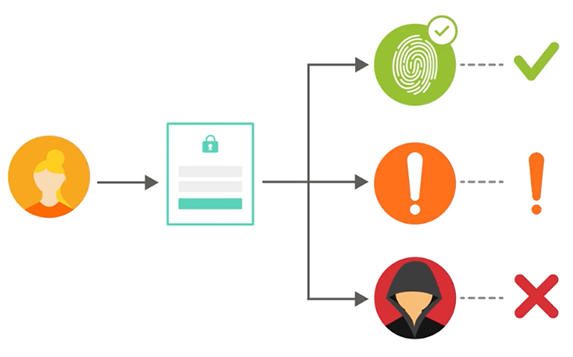

The Account Opening API utilizes a set of network signals that provide insight on the legitimacy of credentials a user inputs when setting up an account to assess the risk of the customer onboarding in process.

Account Opening API

Onboard more customers with higher confidence and lower friction.

Identify potential bad actors

Identify stolen or fabricated information during the account building process to identify and prevent fraud.

Reduce friction for legitimate customers

Streamline your user registration process to validate legitimate customers and fast track their approval to onboard or transact.

Improve trust and safety within your platform

Prevent illegitimate access to your platform with a sound frictionless fraud prevention approach that accurately validates users.

Resources

Blog

Understanding synthetic identity fraud: Challenges and solutions in the digital age at Mastercard Identity Connect London

Report

Does your identity verification workflow detect synthetic identities?

CONTACT AN EXPERt

Contact us to find out how our solutions can help reduce fraud risk for your business.